March Market Madness

All,

Welcome and thank you for subscribing to the Lefty Group monthly newsletter! The content of the letters will provide you with monthly updates on current economic and market conditions, what the fund is doing and what you should be considering in your own private wealth accumulation journey!

These newsletters are meant to be informational and educational only. They are not financial advice, and I am not a financial advisor. Always do your own research before investing any of your hard-earned money into something!

Monthly Highlights

· One Year Anniversary of COVID-19 Pandemic Declaration

· Big Vaccine Push

· Stimmie’s!

· The Federal Reserve & Inflation Expectations.

· 10-year Treasury Yield Surges

· Why We Bitcoin

COVID Anniversary

On March 11, 2020, the World Health Organization declared COVID-19 a global pandemic. In one year since that declaration, we have seen the pandemic play out in epic fashion with nearly 550,000 Americans dead, full scale lockdowns, protests, unprecedented amounts of government stimulus and a stock market crash with a subsequent recovery. All this while businesses nationwide have closed their doors for good and millions of Americans remain unemployed.

While the pandemic has raged, the nation has experienced large scale protests against police brutality and racial inequalities, a Presidential election the likes of which have not been seen before, and an attack on the American capital. It really is tremendous to reflect on the past year and remember all we have experienced together as a nation.

The Big Vaccine Push & Re-openings

Not all is bad though. As of writing there are several vaccines being distributed for use world-wide with three authorized for emergency use in the United States right now. The U.S. has already vaccinated nearly 15% of the population with millions more adding to this percentage daily. Currently America is tracking roughly 3 million shots per day.

In addition to this, President Biden indicated on March 11th that all Americans will be eligible to receive the vaccine starting May 1st. This is great news as communities and businesses are slowly able to open with a greater sense of safety bringing things ever closer to a sense of normalcy. Whether agreeable or advisable, nationwide some states have already began easing capacity restrictions and mask mandates allowing their economies to fully re-open. While I do believe we should listen to the scientists and doctors urging us to continue to wear masks and get vaccinated, I also believe we are at a point where re-opening the economy and schools can be done so in a responsible way.

There is no denying there is a lot of pent-up demand for seeing family, socializing with friends, traveling, and going to events like concerts or sporting events. With a May 1st nationwide eligibility these events at a larger scale seem likely possible very soon. Naturally, there will be capital expenditures to fund these activities.

On the surface it seems likely that the market would benefit from increased spending, sending stock prices up accordingly. While there is some truth to that, and the market can definitely continue to benefit from some stability in revenue and forecasting profitability, the market is also a forward-looking entity. What that means is that the market is always looking 6-12 months ahead of the current economic situation. Evidence of this became clear throughout 2020 as the market began to price in a recovery with optimism around vaccines, re-openings, and more stimulus, subsequently recovering off it is lows last March ending the year higher. The benchmark S&P 500 index ended pandemic-hit 2020 with gains of 16.3% while the Nasdaq ended the year up a whopping 47%.

For someone unfamiliar with financial markets it is almost unfathomable to think the stock market could end the year higher than where it started in the midst of a global pandemic. While the market’s forward-looking mentality surely played a part in the recovery, there are numerous other factors that have contributed to the snap back which will be discussed below.

Before moving on, it is worth highlighting that the rest of the world is not on the same footing as America. Vaccination availability and access differs across the world with a lot of countries not catching up to America’s progress until 2022-2023 and beyond.

Within the month of March, we have seen a pause in the U.K.’s AstraZeneca vaccine putting a damper on optimism surrounding the European recovery. In addition to this, we have seen Hong Kong halt vaccine use in Pfizer/BioNTech’s vaccine hampered by packaging concerns.

COVID will continue to be prevalent around the world and its prevalence in each country will be reflected in their economies. More so, we are starting to see European countries experiencing new surges in cases, with extensions of lockdowns in Germany also announced this month.

It is important for Americans to remember this while making travel plans and/or looking at international investments. Whether you are vaccinated or not, traveling to another country will pose a risk to its citizens and potentially yourself.

2020 Beneficiaries & 2021 Winners

The Nasdaq technology and stay at home names benefited tremendously from the work-from-home environment in 2020. Companies were forced to quickly shift and adapt to the remote work environment. Nasdaq names like Zoom, Peloton, Slack, Teladoc and Roku (among many others) saw a significant rise in their share prices while the Dow Jones Industrial and Russel 2000 cyclical and small cap names like industrials, energy, oil, banks, airlines, hotels, and restaurants struggled with weak demand.

Into the later half of last year, particularly after the November 3rd presidential election, we began to see more optimism around the cyclical and small cap names. With a Democrat controlled government, the market began to price in a substantial recovery, a large stimulus package, and more recently full-scale re-openings with market participants to rotating away from high valuation technology stocks and into value.

The rotation into industrials, energy, airlines, and other names that benefit from an open economy began to really pick up steam in late February and through the past month of March as it became clear a large stimulus bill would be passed along with a government committed to large scale vaccination efforts. However, any unforeseen setbacks like a large spike in COVID cases or re-opening delays will surely cause some market uncertainty.

Over the past month the Dow Jones Industrial has risen roughly 6.5% with the Russel 2000 small cap rising about 3%. Comparatively the Nasdaq is about flat for the month, falling over 6% by mid-month, since recovering some of those losses.

Index Year to Date Gains

· S&P 500 +5.5%

· Nasdaq +1.75%

· Dow Jones +7.5%

· Russel 2000 +13.5%

For perspective, the consensus price target on the S&P500 benchmark index is 4,000-4,100 by the end of the year. That represents about 5% upside from current levels. A year end at 4,100 would put the benchmark at about a 9% gain for the year. Shouldn’t the benchmark index with a market in full recovery mode advance more than it did during a global pandemic?

Sure, and the S&P500 index is just one of many indexes that participate in the open market as I mention above. I have no doubt there will be many market beneficiaries that struggled in 2020 that are set to shine in 2021. With a recovery priced in however, the market in 2021 will be much more difficult to navigate. Investors must be strategic and thoughtful when deciding where to park their cash and pay close attention to market factors outside COVID recovery.

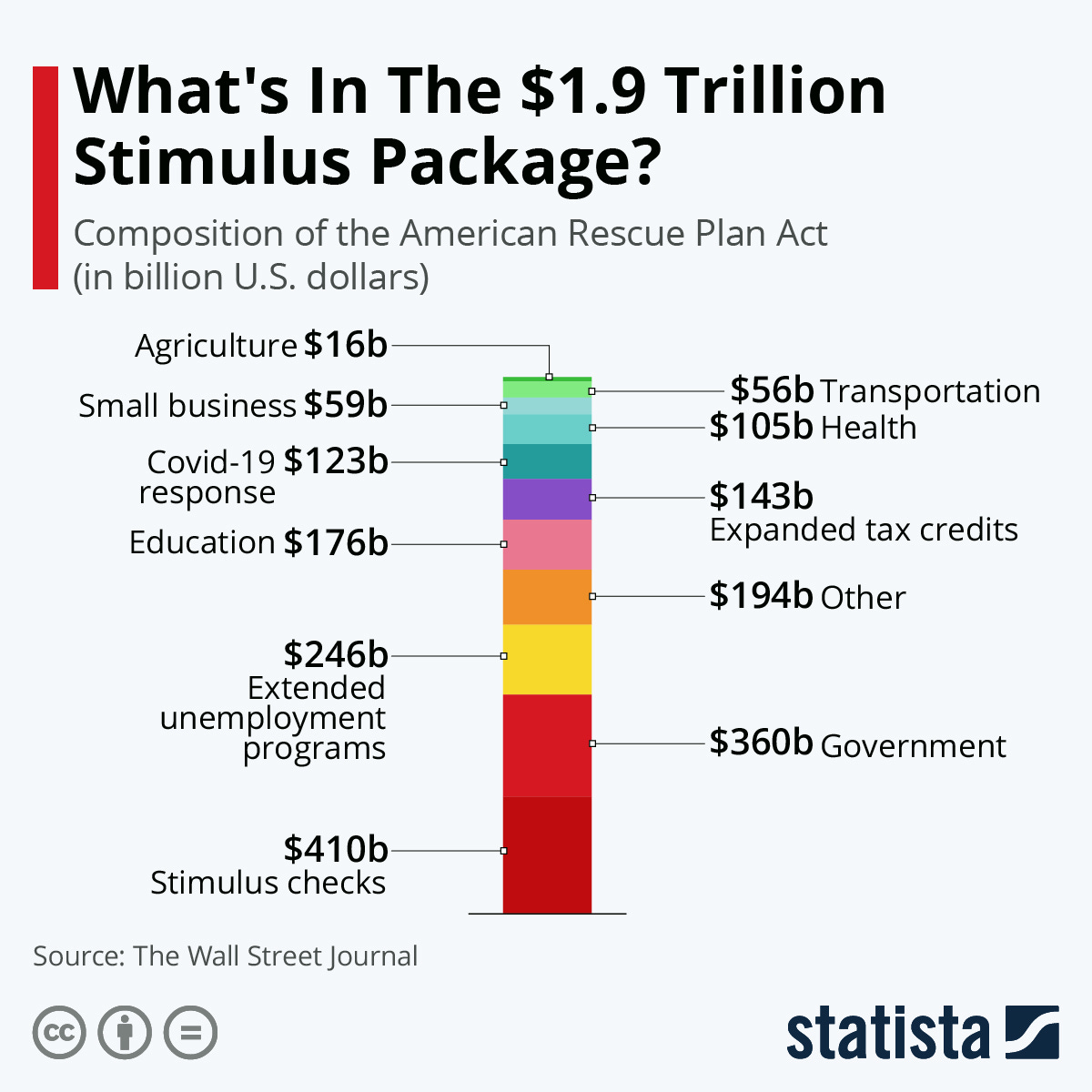

Stimmie’s! – American Rescue Plan is Passed

Speaking of cash, most Americans will have received their $1,400 stimulus payment this month. The $1.9 trillion rescue package was officially signed by President Biden on March 11th.

A total of $410 billion from the package is set to go directly to American families through direct payments. It is estimated that 10-15% of those payments will be invested into the stock market or bitcoin, a total of roughly $40-$60 billion in additional liquidity. Surely the added liquidity will aide in asset price appreciation.

With the passage of the latest rescue package the American government will have provided $5 trillion in stimulus since the pandemic began. That is a lot of cheese.

Warranted or not, there is no such thing as a free lunch. Money must come from somewhere.

For the government, the $5 trillion in stimulus efforts simply came from expanding the monetary supply, printing money out of thin air, thus further increasing the national debt to scary levels.

Unfortunately, most Americans will look at the situation and gladly spend the money given to them for free, not considering the long-term implications expansion of the monetary supply will carry on inflation.

The Federal Reserve Actions

At the start of the pandemic the Federal Reserve deployed several of its own tools to help maintain and control the economy including emergency lending, cutting interest rates and quantitative easing efforts to name a few.

In March 2020, Federal fund interest rates were cut twice to 1.00% - 1.25%, and then again further to 0% - 0.25% shortly after in an effort to stem the damage caused by a halted economy and encourage borrowing through cheap rates. Cheap capital flooded the market.

It is important to understand that the Federal fund rate is the most important interest rate in the world. It uses interest rates as a lever to grow the economy or put the brakes on it. If the economy is slowing, interest rates are lowered to make it cheaper for businesses to borrow money, invest, and create jobs. Lower interest rates also allow consumers to borrow and spend more, which helps spur the economy.

When rates are low, it is considered an expansionary monetary environment.

I do not want to bog you down with extraordinary details of how the Federal Reserve operates, but a basic level understanding is important to have as these operations are instrumental in the creation of inflation and associated market performance.

The Fed manages the fund rate with open market operations. It will buy or sell U.S. government securities (treasury bonds) to Federal Reserve member banks such as Wells Fargo, Goldman Sachs, and Morgan Stanley. When the Fed buys securities, those purchases increase the reserves of the bank associated with the sale. This makes the bank more likely to lend at a cheaper rate with extra cash on hand.

These shifts in the fed fund rate ripple through the rest of the credit markets. They influence other short-term interest rates such as savings, bank loans, credit card interest rates, and adjustable-rate mortgages.

Ok, so exactly what is the Federal Reserve doing here?

The Federal Reserve is not actually printing new money, that is the job of the U.S. Treasury department. Instead, they have been injecting money into the economy through large asset purchases on the open market, adding newly created electronic dollars to the reserves of banks.

These asset purchases are known as quantitative easing (QE). What they are doing is purchasing is large amounts of bonds – U.S. Treasury securities and agency securities that are backed by bundles of home mortgages and bonds from their member banks. It is quite the complicated mess.

At the start of 2020, the Federal Reserves asset balance sheet was at $4.2 trillion. Since that time, the balance sheet has grown to almost $9 trillion with continued expansion on the horizon.

Currently the Fed is projected to continue this trend purchasing over $120 billion in additional Treasury securities every month through 2021. That is an additional balance sheet expansion of over $1.4 trillion. Since the pandemic began a year ago, the Federal Reserve in coordination with the American government, has run up the national debt level to over $25 trillion with no signs of slowing down.

It is worth noting that quantitative easing efforts were also used in the wake of the 2008 financial crisis to restore stability to financial markets. Post financial crisis, the interest rate was at virtually 0% from December 2008 until December 2015. Then, as the economy picked up steam, the Fed began to raise the benchmark rate, with rates continuing to rise steadily until late 2018.

After a series of increases through 2018, the market responded heavily selling off almost 25% from Oct-Dec 2018 when market consensus became that the Fed raised rates too much too fast. The market forced the Fed’s hand and they reversed course, slowly lowering rates to counteract a weak economy through 2019 and right into the hands of the COVID-19 pandemic.

Monetary Expansion & Inflation

As I will detail below, investors have started to turn their attention away from COVID and towards inflation expectations. This has become apparent through the quick rise in treasury yields since the start of the year, escalating through March.

You cannot have a monetary base expansion without inflation as the consequence. It is estimated that nearly 25% of the current in circulation US dollars were printed since the pandemic began.

However, according to the Federal Reserve, inflation is not yet present in the “data” with 2020 ending at a 1.4% inflation rate. Huh?

Some of the “data” they are referring to is the consumer price index (CPI). The CPI only considers consumer good prices for households such as food, shelter, and clothing. The CPI does not include data for manufacturing, raw materials, or asset appreciation.

This is a problem because the increase in monetary supply does not only show up in consumer goods prices, but also affects asset prices like stocks, bonds, real estate, art, etc. In the last decade, central banks' inflationary policies have shown up predominantly in rising asset prices and not in sharp increases in consumer prices.

It should be clear that a rise in asset prices erodes the purchasing power of money just as effectively as an increase in consumer goods prices does. Nevertheless, central banks defend the idea of measuring inflation in terms of changes in consumer goods prices but not asset prices.

Here is some 2020 data not being considered by the Fed:

· Corn +35%

· Wheat +25%

· Soybeans +50%

· Lumber +110%

· Copper +32%

· NASDAQ +47%

· S&P500 +16%

· Real Estate +20%

· Bitcoin +310%

· Ethereum +500%

There is good reason to believe that the loss in the purchasing power of money is much higher than is suggested by consumer goods price statistics. For instance, in the period from 2000 to 2019, the US dollar has lost 35% of its purchasing power compared to consumer goods prices. In the same period, it has also lost 53% percent of its purchasing power in terms of housing.

In other words, people have to spend more than double the amount of money on a house today compared to twenty years ago, or they have to save twice as long or borrow twice as much.

Not only does monetary expansion help the rich get richer as their assets appreciate drastically, but it dis-appropriately hurts the poor and middle class as the money they do have is eroded away with inflation, making purchasing a home, saving money, and investing in price appreciating assets further and further out of reach.

Those free stimmy checks don’t seem so nice now, do they?

Biden Infrastructure Plan & Taxes

Whispers of an infrastructure plan in the works have also begun to circulate this past month. It is estimated the proposed plan will be $3 trillion.

Again, whether warranted or not, that is an additional monetary expansion of $3 trillion the American people will have to pay for.

On March 23rd and 24th Fed Chief Jerome Powell testified before Congress on the feasibility of the package and how it may affect inflation. True to the Fed’s distorted view on the measurement of inflation, it was indicated it would not significantly affect inflation projections.

Investors should keep an eye out for further developments on the proposed plan and how it will be paid for. The most likely scenario will be proposed tax increases on Americans to help offset the cost. Also, do not be surprised to see arguments for a tax increase emerge to help fund the spending of the numerous COVID stimulus packages.

Current Federal Reserve Outlook

We heard from Fed Chief Jerome Powell several times over the past month. During its March 2021 FOMC meeting, Powell indicated it would maintain its target for the federal funds rate at a range of 0% to 0.25% until 2024 and until inflation is at 2% for the long term. Simply put, they will allow cheap, easy to borrow capital to continue to flood the market for the foreseeable future.

In addition, the Fed will allow inflation to run “hot” and rise above 2% in the short term to achieve maximum employment. In a revision upward, the Fed communicated that it expects inflation to increase to 2.4% this year as the economy recovers with a subsequent drop to 2.0% in 2022.

Again, keep in mind this is all based off the consumer price index data (CPI).

In my opinion, in all likely hood inflation will rise drastically above the 2.4% target in the years to come and by the time it is present in the Fed’s “data” I fear it will be too late to curb the rise in prices. The Federal Reserve will desperately try to raise rates to offset the inflation and Congress will act to raise taxes.

Large scale projects and capital expenditures undertaken with cheap debt by companies assumed to be sound will be rendered unprofitable due to a sudden rise in the price of goods and interest rates. The sudden rise in prices will cause stalls or abandonment in these projects. With projects nationwide abandoned, a rise in unemployment will occur simultaneously. This economy wide failure of overextended businesses is called a recession.

This is where we are at today. Endless government printing of money and artificially low interest rates. Central banks have pinned themselves into a corner and are simply delaying the inevitable recession to come. As soon as the government started down the path of inflating the money supply there was no escaping the negative consequences. If they stop, inflation and interest rates will rise, and a recession will follow.

When that will occur, I cannot say. Inflation can be kept artificially low for long periods of time through manipulation of the CPI data while assets like stocks, real estate, bitcoin, art, etc. will continue to appreciate.

It is up to you to be mindful of the economic and monetary policy reality we live it. More importantly, it is essential to consider investing your money into assets that will continue to appreciate in this environment.

The 10-year Treasury Yield

What does all this mean for the markets moving forward?

Well, take a look at what the U.S. Treasury bond yields are saying.

U.S. Treasury yields are directly related to interest rates and inflation expectations. Inflation is a bond's worst enemy. Inflation erodes the purchasing power of a bond's future cash flows.

The higher the current rate of inflation and the higher the expected future rates of inflation, the higher the yields will rise across the yield curve, as investors will demand a higher yield to compensate for inflation risk.

Despite statements from the Fed that inflation risk remains low, U.S. treasury yields have begun to surge drastically in 2021 with the 10-year treasury currently jumping to as much as a 1.75% yield, a 14-month high. The 10-year yield began the year just under 1%. Analysts are now projecting the 10-year to hit a 2.25% yield by year’s end.

What this move says is that the market does not like the idea of inflation running hot above 2%. Reactions indicate that markets either see longer-term risks to inflation, or near-term risks of the Fed wavering from their stated approach to keep rates low through 2023.

Equity Market Perspective

With the drastic rise in yields, equity indexes like the Nasdaq and S&P500 have been quite volatile through March. High valuations for large cap and technology companies are being questioned as investors are tempted to park cash in “safer” higher yielding treasuries. Higher yields coupled with a rotation away from growth and into cyclical and value make the winners of 2020 less attractive. Nonetheless, we are in a monetary expansion and inflationary environment. Assets and equities will continue to rise across the board, high growth and technology included. Investors must be selective weighing various factors in their decisions.

This is Why We Bitcoin

“Looks like a million bucks!” - I am sure you have heard the phrase before. Coined in the early 1900’s, the term itself has quite a few connotations, including many that have been ingrained in us since we were children. Becoming a “millionaire” meant being set for life, and not having to worry about things like personal finances again.

Unfortunately, that is no longer the case. To have the purchasing power of a millionaire from the 1900’s, you would need at have nearly $30 million in today’s dollars! In addition, to have the same impact or influence on the economy as a millionaire from the 1900’s, you would need closer to $100 million in today’s dollars.

What is worth $10 today will be worth less in the future. An item purchased for $1 in 2015 now costs about $1.11 in 2021. Talk about currency devaluation.

Although I have specifically wrote about America in this newsletter, monetary expansion and inflation are the root cause for currency devaluation world-wide.

I employ you to look into hyperinflation that has occurred in countries like Venezuela where a month’s wages are equivalent to buying a hotdog in America, or Turkey where the value of the Turkish Lira has fallen 15% over the past month due to government policies.

In the past, savvy investors have turned to gold as a store of value hedge against inflation. In the current digital age, the proper hedge against inflation and poor government policies is bitcoin.

Gold is heavy, tough to move in large quantities and most of it is locked up in central bank vaults. In addition to this, we cannot say with 100% certainty the amount of gold that exists in the world, making its scarcity questionable.

On the other hand, bitcoin is a provably scarce digital asset that cannot be diluted. It is a highly secure decentralized network that is free from central bank policy manipulation and politician’s short-term agendas.

In my opinion, it is absolutely imperative to understand bitcoin’s importance in today’s society along with a non-zero exposure to the emerging digital asset.

I look forward to diving deeper into the importance of bitcoin in future newsletters. In the meantime, you owe it to yourself to do some critical research on the asset to protect and grow your wealth.

Expand your Bucket!

It is a pretty common theme that people who come into wealth suddenly have a tough time keeping that wealth. There have been far too many stories of lottery winners, athletes, actors, and musicians who have gone broke after making millions. It is also pretty common for people who make significantly more than others at a job to be broke in comparison. But why is that?

Imagine your ability to maintain wealth as a bucket in which you carry with you. Each dollar earned is equivalent to a drop of water. For most people, they may carry around a 12oz bucket in which the money they make is stored and any extra simply spills over the edges, gone forever through wasteful spending.

For lottery winners or athletes carrying around a 12oz bucket, dumping 100 gallons of water on their lap usually results in water spilling all over the floor. This can be seen through large and expensive purchases of houses, cars, etc.

Before long, those 100 gallons are spent, and the lucky lotto winner is right back to carrying around a 12oz bucket.

Only through financial literacy can that bucket be expanded.

Set up budgets for yourself, restrict large and unnecessary purchases, read books and educate yourself on money management. Those things are key to expanding your bucket.

When you spend time on your financial literacy, your bucket has the capacity to expand from a 12oz cup to a 5-gallon jug and furthermore to barrels and tanks of large proportions. Suddenly, the water that used to spill over the edges of your bucket’s limitations is now being captured and stored effectively, allowing you to actually accumulate wealth.

Over time, investing in assets or making large purchases such as a house or a car become more obtainable as you can hold onto and grow your wealth. Expenses that previously drained your 12oz cup can now be thoughtfully spent with less of an impact to your larger vessel. If you cannot manage $1,000 effectively you will never be able to manage $100,000 effectively.

We live in an age where education and information on anything we want to know is accessible at our fingertips through the internet. You owe it to your future-self to become educated in money management.

By signing up for this newsletter you have already taken steps to accomplish that. Stay consistent on your journey and don’t stop learning.

I cannot thank you enough for spending the time to read the first edition of the Lefty Group newsletter.

I look forward to sharing additional thoughts and perspective on economic and market outlooks along with money management tips and tricks to aide in your individual journeys.

P.S. if you like what you read here, please share with your friends and family!

Bryan Craig

Lefty Group Capital Chief Investment Officer