Fourth Quarter Financial Conditions

Fourth Quarter Financial Conditions

September 2021 #7

Hey!

The last three months of the year (aka the fourth quarter) are about to get really interesting for financial markets. There is a lot of anticipation building in numerous areas as several key decisions/outcomes are expected to play out over the coming months. Are we setup to crash and burn as a whole or can gains continue to be expected?

Up until the start of September it’s been a great year for financial markets. After nearly a year without a 4.5% downside monthly move in the S&P500, September gave us just that. We are currently closing out the month down right around 4.5% with strong downside pressure coming in over the last week.

Let’s talk about the various market factors in play and what you should be thinking about in this environment coming into Q4.

First though, these newsletters are meant to be informational and educational only. They are not financial advice, and I am not a financial advisor. Always do your own research before investing any of your hard-earned money into something!

Letter Highlights

· Federal Reserve Tapering Expectations

· Fed Credibility Questioned

· US Default Risk

· Is it Bitcoin’s Time to Shine?

Index Year to Date Gains Through End of September

· S&P 500 +16.4% (-4% mo./mo.)

· Nasdaq +14% (-5.5% mo./mo.)

· Dow Jones +12.2% (-2.5% mo./mo.)

· Russel 2000 +11.6% (-2.7% mo./mo.)

· Bitcoin +42% (-12% mo./mo.)

· Ethereum +265% (-17.5% mo./mo.)

Federal Reserve Tapering Expectations

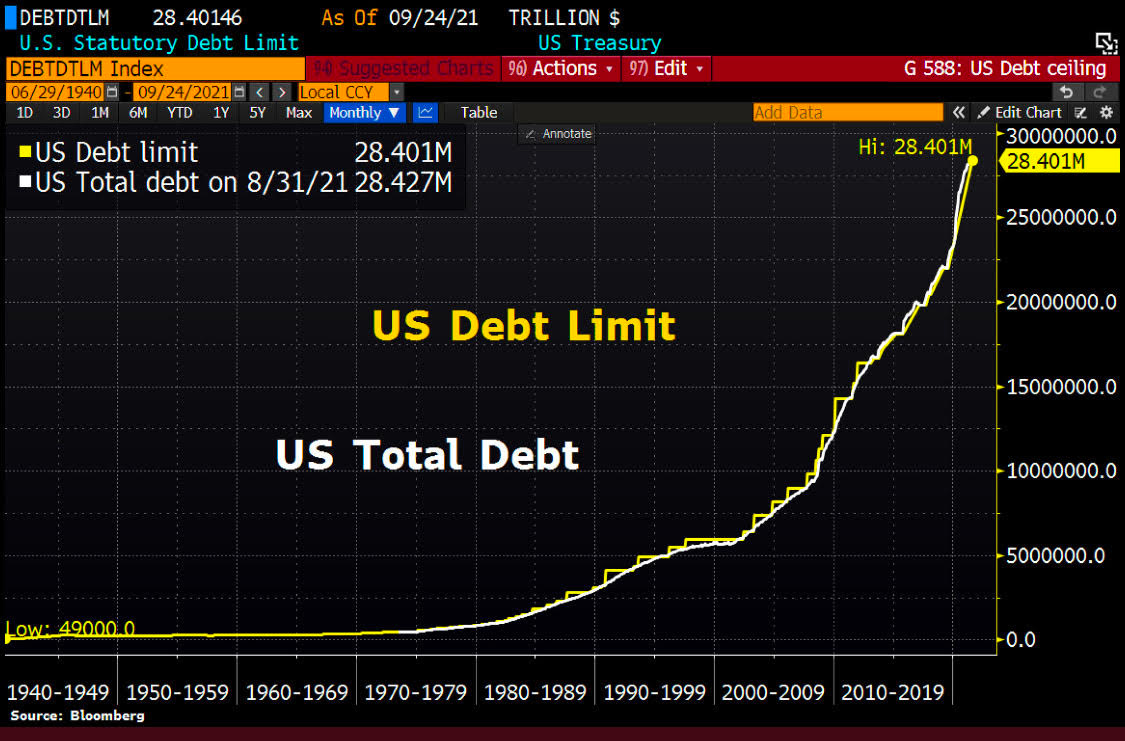

I’ve talked about this a lot, but the U.S. Federal Reserve is a key player in what happens next for financial markets. After stepping in to backstop the collapse of financial markets at the start of the pandemic over 1.5 years ago, the Federal Reserve has continued to pump at least $120 billion a month into the economy through its quantitative easing programs. This has added more than $4 trillion to the Fed’s balance sheet which now stands at $8.5 trillion. US national debt has now expanded to a whopping $27 trillion through quantitative easing and stimulus measures. However, we are slowly being eased into an unwinding of these easy monetary policies through Fed statements and testimonies.

Earlier this month, Fed officials indicated they are almost ready to pull back the stimulus and begin tapering these purchases.

Although, that decision is contingent on inflation and job growth/unemployment conditions being met.

During remarks, Fed Chair Powell stated the official tapering decision could happen at the November meeting and the process would commence shortly thereafter. He also added that he sees tapering being finished “sometime around the middle of next year.”

If the taper indeed begins in December, reducing the purchases by $15 billion a month would get the process down to zero around July 2022. Still, between now and then an additional $650 billion would be injected into the system as QE slowly unwinds.

We already know inflation has more than exceeded expectations. Powell said this himself in statements which further indicated inflation would be more persistent and permanent.

The stated inflation rate is currently at 5.3% based on an extremely flawed CPI metric. In reality it’s much higher.

Nonetheless, without a doubt inflation will remain high hindered by easy monetary supply, supply chain issues and labor shortages.

With inflation expectations clearly met, the other side of that coin is jobs growth and unemployment. We know unemployment benefits have begun to roll back this month, however so far jobs growth remains slow to stagnant at best.

Data released for August shows the economy created much fewer jobs than expected, bringing in a total of 235k versus the expectation of 750k, with the unemployment rate remaining elevated at 5.2%. That’s a big miss and it was blamed primarily on the Delta variant.

It looks like the Jerome Powell and the Fed are hanging their hat on a big return to work starting this month with unemployment rolled back and the Delta wave seemingly peaking. We shall see over the coming weeks when additional jobs data is released for September.

I tend to think jobs growth will remain slower than anticipated the rest of the year.

Companies are now optimized for remote work, have streamlined their operations and inefficient employees are mostly gone. Not to mention the lack of people actually wanting to return to work without a hefty pay increase and as we head into the winter months fearful of another pick up in COVID.

A slower than anticipated return of the workforce could definitely throw a wrench in the Fed’s tapering plans. This can be good and bad for markets.

The market has gotten drunk on the easy monetary environment with asset prices rising significantly. A delay on tapering would allow this continue, further skewing the already inflated asset prices.

Any enthusiasm might be short lived though as investors realize labor shortages and supply chain issues may persist, impacting businesses and revenue potential, not to mention overall economic growth.

This becomes a problem when valuations are already starting to become questioned. The longer the charade goes on the worse it’ll eventually be. The best outcome for markets would be a gradual taper to start in December as projected by the Fed.

In my opinion the market has begun to digest this path forward. This was evident leading up to the FOMC meeting earlier this month as we saw a shift in sentiment.

Markets began to sell off leading up to the event anticipating an announcement of a taper starting in October, only to reverse once the anticipated path forward for later this year became most likely December. That gave the market an opportunity to swallow the pill of an eventual attempt at normalization in due time.

If jobs growth remains stagnated too long though and the Fed delays tapering plans, market sentiment could sour as monetary expansion and inflation would continue to persist. A calculated return towards a balanced environment would ease market nervousness into 2022.

Fed Credibility Becoming Questioned

Outside monetary policy concerns, all sorts of other craziness has emerged questioning the credibility and ethics of the U.S. Federal Reserve and its members.

First, just this week two top Fed officials (Eric Rosengren and Robert Kaplan) resigned in wake of financial disclosures revealing extensive stock trading in 2020 all while the Fed was spending trillions to stabilize markets.

Because of their trading, without a doubt the two officials definitely profited from the Fed's actions, a clear conflict of interest. The ethical framework of the Fed’s rules for market participation is now coming into question with potential rule changes and investigations occuring.

Further fueling the fire on the Fed was Senator Warren calling out Jerome Powell directly at a senate hearing this week.

“Your record gives me grave concerns. Over and over, you have acted to make our banking system less safe, and that makes you a dangerous man to head up the Fed, and it’s why I will oppose your renomination,” Warren said.

Senate comments today hint that the shift in inflation is not just 'not transitory' but could be 'structural' and more permanent than led to believe. This realization could prompt many to adjust expectations for an even more aggressive Fed action on tapering.

Take away the support too quickly though and markets will sour just the same. Whether this puts temporary pressure on markets or not, I believe a gradual easement of Federal support would benefit the long-term health of the system. Keep an eye out for increased pressure on the Federal Reserve to act.

U.S. Default Risk Fears

Late Monday, Senate Republicans blocked a bill to fund the federal government until Dec. 3 and raise the debt ceiling. With Treasury Secretary Yellen testifying before the Senate Banking Committee this week, Yellen warned Congress must raise the debt limit by Oct. 18.

"It is imperative that Congress swiftly addresses the debt limit. If it does not, America would default for the first time in history," Yellen said. "The full faith and credit of the United States would be impaired, and our country would likely face a financial crisis and economic recession."

Obviously, this cannot occur. America defaulting on its debt would be catastrophic for world markets and is not really an option. The debt ceiling is inevitability going to get raised or just flat out removed. Until then though, the market will take the uncertainty as a risk and may continue to show signs of weakness and downside as it has this past week.

The ability for the US to pay its debts is laughable. It won’t happen. For the record, the government has collected a record amount of federal income tax revenue every single year since 2009. Each year they collected more tax revenue than the year prior, yet the deficit has continued to increase.

The US doesn't have an income problem, we have a spending problem.

Don’t forget there is a $3.5 trillion infrastructure package that is trying to be pushed through as well. The fact of the matter is that debt will continue to increase to fund the government’s endeavors.

My anticipation is that politicians on both sides will continue posturing as they still are fighting to incorporate this infrastructure package. Ultimately the debt ceiling will be resolved at the last minute and markets can take a breath. This uncertainty will definitely keep the markets on its toes in the meantime though.

Is it Bitcoin’s Time to Shine?

The stage is set for bitcoin and broader crypto to have a big Q4 to end the year for several reasons.

First, a lot of the monetary and government debt issues play right into what bitcoin is about and why it’s important. It was created as a response to the 2008 financial crisis which is starting to look miniscule compared to today’s issues.

I think the realization that government debt, the US dollar supply, and inflation will pretty much continue to go up forever will continue to draw people to bitcoin for its scarcity properties and the fact that its an open monetary network free from government debasement. Although this may be a longer-term realization for many, implications over the coming months will matter.

Historical data shows that within the four-year bitcoin cycle, approximately 18 months after a bitcoin halving occurs the asset sees significant price appreciation in a short span of time. This happens to fall in Q4. History doesn’t always repeat but sometimes it rhymes. Comparison of past cycles vs. today can be seen below.

This thesis is further supported through some of the following examples of current on-chain data analytics.

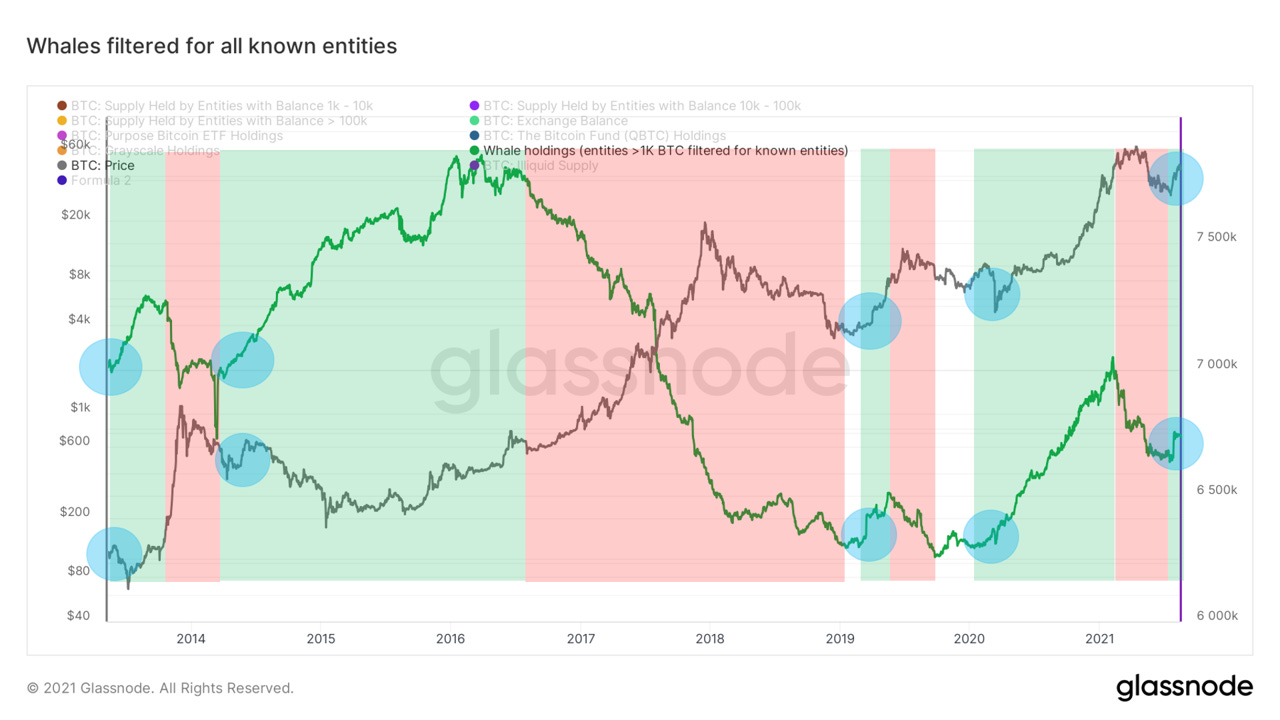

One, whales (large players) are buying and have been since mid-July. When zooming out, we can see that following the trends of whales has been a viable idea. These big players tend to buy early on in broader uptrends and begin selling into strength.

Two, minnows (the little guys) have also been buying. When we zoom out looking at the portion of supply held by retail, we see that their holdings are currently amidst a large increase, similar to the middle of each prior major price uptrend.

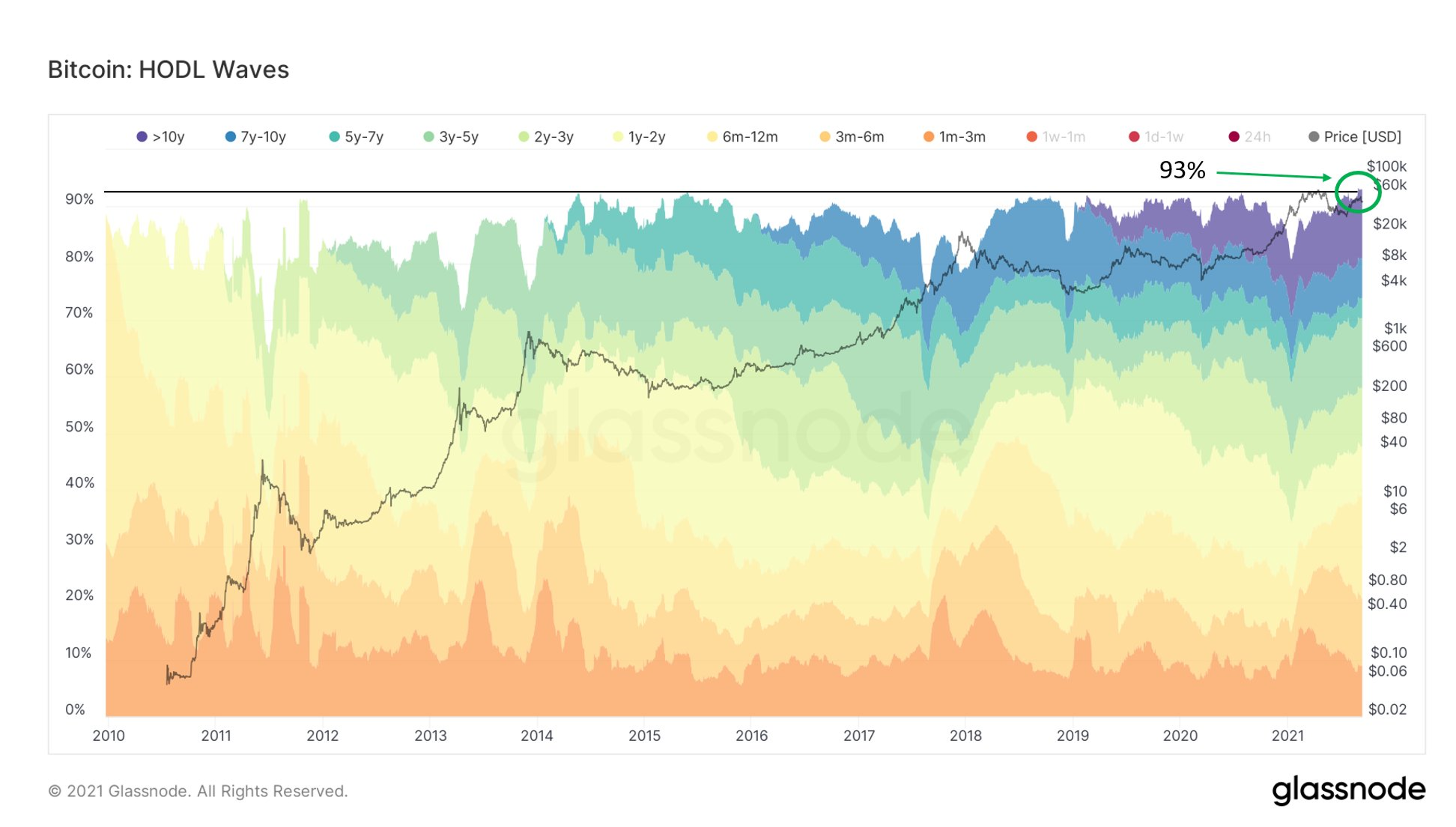

Further, HODL waves which show the portion of supply that hasn’t moved in various time cohorts indicates that 93% of the supply hasn’t moved in at least a month, this is an all-time high. Another way to think of this is the amount of supply that is actively being traded is at an all-time low. Entities with low spending behavior are continuing to lock up coins.

Another potential bullish catalyst is the approval of a bitcoin ETF for trading on exchanges. There are currently over 30 applications under review by the SEC for approval. A single approval of an ETF in the U.S. would allow a tremendous amount of sidelined investor capital to pour into the space.

Many institutions and investment firms are stuck sidelined until the SEC gives the greenlight. Numerous countries world-wide already have approved bitcoin ETFs for trading, including our neighbor to the north, Canada. At what point does the SEC realize they are missing out on an opportunity?

Given the review periods from the data of submission, the SEC could approve an ETF as soon as late October with several more shortly after. That would be massively bullish.

In other massively bullish news, El Salvador has officially made bitcoin legal tender in their country. Which nation state will be next to join? Game theory is now fully in motion.

Also massively bullish is the announcement of Twitter’s integration to the bitcoin lightning network. Instant payments through twitter can now be made to anyone using the BTC network for free and automatically converted back to the currency of your choice. Check this out! Western Union is screwed!

There are broader risks though. The SEC has been very cautious on the broader crypto space. Particularly many tokens, de-fi projects, centralized exchanges, and altcoins (not bitcoin) could be regulated heavily and many speculators could get hurt. Calls for SEC clarity on a framework for the crypto space continue to grow louder.

A clear guideline provided by the SEC would allow many of these large institutions to make investments into the space. Definitely something to pay attention to as I expect the SEC to move soon on the still very unregulated space.

Outside regulatory risks, once bitcoin starts moving the broader industry will move too as I have said before.

Final Thoughts

September is historically a weak month. As we wrap up the month in the red, look for the market to try to find some footing in October as debt ceiling concerns ease.

The U.S. monetary policy remains one of the key factors for the market’s direction as we head into 2022. A strong jobs recovery and successful tapering plan would be a healthy thing for the market’s durability although it may cause a bit of volatility as things shake out.

I am looking for a lot of positive developments in the crypto space as we work through Q4. Do your research and know the risks associated before risking any of your own money.

We live in an age where education and information on anything we want to know is accessible at our fingertips through the internet. You owe it to your future-self to become educated in money management.

By signing up for this newsletter you have already taken steps to accomplish that. Stay consistent on your journey and don’t stop learning.

Catch ya later!

Bryan Craig

Lefty Group Capital Chief Investment Officer

(P.S. if you like what you read here, please share with your friends and family!)